")

Saving your first $1,000 is one of the most important financial milestones you can reach. Many people search how to save your first $1,000 because building that first financial cushion creates stability and reduces dependence on debt.

A $1,000 starter emergency fund can help cover unexpected expenses like car repairs, medical bills, or sudden travel. Without savings, many people rely on credit cards or personal loans.

According to the Federal Reserve, nearly 37% of Americans would struggle to cover a $400 emergency expense without borrowing or selling something. That statistic highlights how critical even a small savings buffer can be.

Learning how to save your first $1,000 isn’t about extreme frugality. It’s about building systems that make saving automatic and consistent.

Table of Contents

- Why Your First $1,000 Matters

- Step 1: Know Your Starting Point

- Step 2: Use the 50/30/20 Budget Rule

- Step 3: Automate Your Savings

- Step 4: Cut One Expense Temporarily

- Step 5: Boost Your Income Short-Term

- A Simple Timeline to Save Your First $1,000

- What Financial Experts Say About Emergency Savings

- What to Do After You Save Your First $1,000

- Frequently Asked Questions

Why Your First $1,000 Matters

When you save your first $1,000, it functions as a starter emergency fund. It’s not meant to cover months of living expenses yet, but it creates financial breathing room.

When unexpected expenses happen — and they always do — your savings prevent a small problem from becoming a financial crisis.

Examples where a $1,000 emergency fund helps include:

- Car repairs

- Urgent medical expenses

- Travel emergencies

- Appliance replacement

- Short-term job gaps

The Bureau of Labor Statistics reports that the average American household spends over $6,000 per year on unexpected expenses. Without savings, those costs often turn into high-interest debt.

Your first $1,000 creates the foundation for long-term financial stability.

Step 1: Know Your Starting Point

Before saving money, you need clarity on where your money is currently going.

Review the last 30–60 days of spending across your bank accounts and credit cards. Categorize expenses into:

- Fixed expenses (rent, insurance, utilities)

- Variable spending (groceries, restaurants, shopping)

- Subscriptions and recurring charges

Many people discover they are spending hundreds of dollars each month on things they barely notice.

Even identifying $100 per month in wasted spending can significantly accelerate your savings.

If you’re unsure how much you should save overall, you may want to read our guide:

How Much Money Should You Save Each Month

That article explains realistic savings benchmarks.

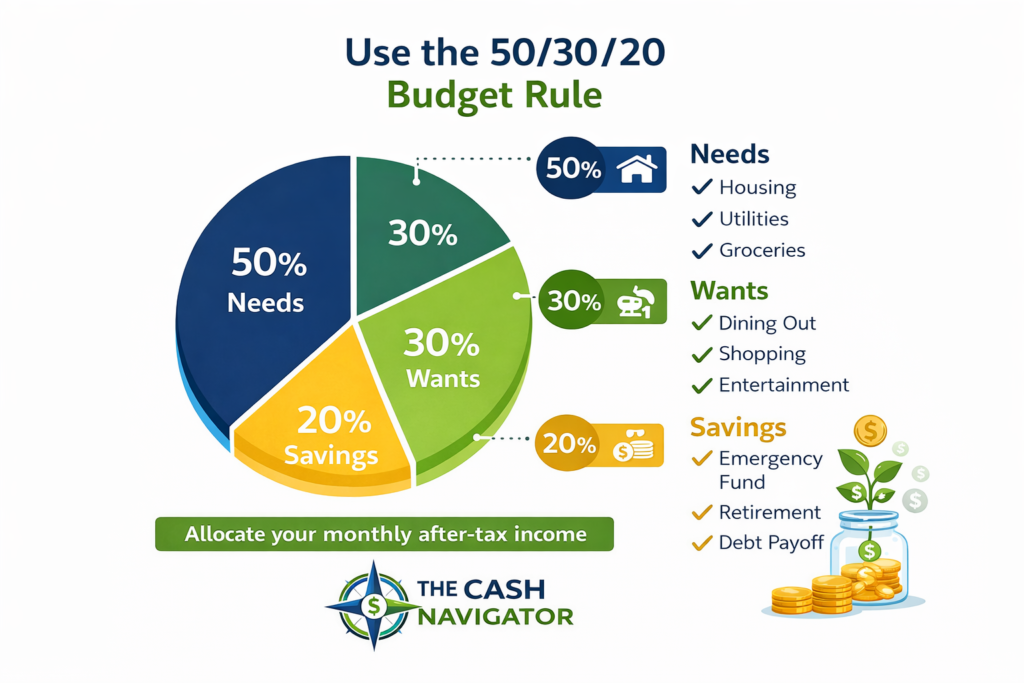

Step 2: Use the 50/30/20 Budget Rule

One of the simplest systems for managing money is the 50/30/20 budget rule.

It divides your after-tax income into three categories:

- 50% for needs (housing, groceries, transportation)

- 30% for wants (entertainment, dining, travel)

- 20% for savings and debt repayment

If you allocate even part of that 20% toward a starter emergency fund, you can reach $1,000 surprisingly quickly.

For a deeper breakdown, see our article:

Live Happy Using the 50/30/20 Budget Rule

This framework helps you maintain balance between spending and saving and put you closer to save your first $1,000.

Step 3: Automate Your Savings

Automation is one of the most powerful financial tools available.

Instead of saving whatever is left at the end of the month, move money into savings immediately when your paycheck arrives.

This method is often called “paying yourself first.”

You can automate savings by:

- Setting recurring transfers from checking to savings

- Using employer direct deposit split into multiple accounts

- Using banking apps that round up purchases into savings

Even small automatic transfers can create momentum.

For example:

- $25 per week = $1,300 per year

- $50 per week = $2,600 per year

Automation removes the temptation to spend money before saving it.

Step 4: Cut One Expense Temporarily

Saving your first $1,000 often happens faster when you temporarily reduce a single spending category.

Instead of cutting everything, focus on one area for 60–90 days.

Examples include:

- Pausing restaurant spending

- Canceling unused subscriptions

- Reducing impulse online purchases

- Cooking at home more often

If you normally spend $150 per month eating out, redirecting that money toward savings could help you reach your first $1,000 in just a few months.

If your income is limited, you may also want to read:

How to Save Money on a Low Income

That guide focuses on strategies for tight budgets.

Step 5: Boost Your Income Short-Term

Cutting expenses helps, but increasing income can accelerate your savings dramatically.

Many people save their first $1,000 by temporarily adding small income streams.

Examples include:

- Freelance work

- Selling unused items online

- Rideshare or delivery apps

- Pet sitting or tutoring

- Overtime hours

Even earning an extra $100 per week means reaching $1,000 in about 10 weeks.

The Bureau of Economic Analysis reports that personal income in the U.S. continues to grow modestly each year, but many households rely on side income to increase savings.

A Simple Timeline to Save Your First $1,000

Here is a realistic savings roadmap.

If you save:

$50 per week → $1,000 in 20 weeks

$75 per week → $1,000 in 13 weeks

$100 per week → $1,000 in 10 weeks

$200 per week → $1,000 in 5 weeks

Small, consistent progress builds momentum quickly.

The key principle behind how to save your first $1,000 is consistency, not perfection.

What Financial Experts Say About Emergency Savings

Many well-known financial experts emphasize the importance of a starter emergency fund.

Legendary Investor Warren Buffett famously said:

“Do not save what is left after spending, but spend what is left after saving.”

Many financial planners recommend building a $1,000 starter emergency fund first, then expanding it later to 3–6 months of expenses.

This approach prioritizes stability before investing aggressively.

If you’re in your early career stage, you may also benefit from this guide:

How to Start Saving Money in Your 20s

Your 20s are often the most powerful decade for building financial habits.

What to Do After You Save Your First $1,000

Once you reach your first $1,000 savings milestone, your next financial goals typically include:

- Expanding your emergency fund to 3–6 months of expenses

- Paying down high-interest debt

- Increasing retirement contributions

- Investing consistently for long-term growth

Your $1,000 starter fund should remain accessible in a high-yield savings account rather than invested in volatile assets.

Liquidity matters for emergencies.

Frequently Asked Questions

Is $1,000 enough for an emergency fund?

$1,000 is considered a starter emergency fund. It helps cover smaller unexpected expenses while you build toward a larger savings goal.

How fast should I save my first $1,000?

Many people save their first $1,000 in 3–6 months, depending on income and spending adjustments.

Where should I keep my emergency fund?

A high-yield savings account is usually the best place. It keeps money accessible while earning some interest.

Should I invest before saving $1,000?

Most financial planners recommend building a small emergency fund first before investing. This prevents needing to sell investments during emergencies.

Final Thoughts

Saving your first $1,000 is one of the most powerful financial steps you can take. It creates stability, reduces stress, and protects you from unexpected expenses.

The most important part of how to save your first $1,000 is consistency. Small habits — automatic transfers, reduced spending, and occasional side income — can add up faster than most people expect.

Once you reach this milestone, continue building your financial foundation by expanding your emergency fund and increasing long-term savings.

Your future financial stability begins with the first $1,000.