A Simple Way to Take Control of Your Money

Managing money can feel complicated, especially with rising housing costs, inflation, and everyday expenses. The 50/30/20 budget rule is one of the simplest and most practical ways to structure your finances.

Instead of tracking dozens of spending categories, the 50/30/20 budget rule divides your income into three clear buckets: needs, wants, and savings.

For many people, this system provides a straightforward starting point for building financial stability.

If you’re still figuring out how much you should be saving each month, you may want to read our guide on How Much Money Should You Save Each Month, which explains savings benchmarks in more detail.

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a budgeting framework that divides your after-tax income into three categories:

50% for needs

30% for wants

20% for savings and debt repayment

This rule was popularized by U.S. Senator Elizabeth Warren in the book All Your Worth: The Ultimate Lifetime Money Plan.

The idea is simple: instead of micromanaging every expense, you control the big picture.

This approach works because it balances three essential financial priorities:

- Covering essential living expenses

- Maintaining a reasonable lifestyle

- Building long-term financial security

How the 50/30/20 Budget Rule Works

Under the 50/30/20 budget rule, your income is divided like this:

Needs (50%)

These are essential expenses required to live.

Wants (30%)

These improve your lifestyle but are not essential.

Savings (20%)

This portion builds your financial future.

This method helps prevent two common financial problems:

• Spending too much on lifestyle expenses

• Failing to save consistently

Even if your income is modest, creating structure around spending can significantly improve financial stability.

If you are currently working with a tighter income, our article How to Save Money on a Low Income explains strategies that make budgeting easier.

Example of the 50/30/20 Budget Rule

Let’s look at a simple example.

Assume someone earns $4,000 per month after taxes.

Monthly Budget Example

Income: $4,000

Needs (50%)

$2,000

Wants (30%)

$1,200

Savings (20%)

$800

This $800 savings portion could go toward:

• Emergency fund

• Retirement contributions

• Paying down debt

• Investing

Over time, consistently saving 20% of income can dramatically improve financial security.

*According to the Federal Reserve’s Survey of Household Economics, many Americans would struggle to cover an unexpected $400 emergency expense without borrowing or selling something.

What Counts as Needs in the 50/30/20 Budget Rule?

Needs include expenses required for basic living.

Examples include:

• Housing (rent or mortgage)

• Utilities

• Groceries

• Health insurance

• Transportation

• Minimum debt payments

Housing typically represents the largest category.

According to the U.S. Bureau of Labor Statistics, housing accounts for roughly 33% of average household spending, making it the biggest factor affecting whether the 50/30/20 budget rule fits comfortably.

Data from the U.S. Bureau of Labor Statistics shows that housing is the largest spending category for most American households. If your housing costs exceed 50% of income, the rule may require adjustment.

What Counts as Wants?

Wants are lifestyle expenses that improve quality of life but are not essential.

Examples include:

• Dining out

• Streaming services

• Travel

• Shopping

• Entertainment

• Upgraded phone plans

Many households unintentionally allow wants to expand over time. The 50/30/20 budget rule helps keep lifestyle spending under control.

This category often provides the most flexibility when trying to increase savings.

What Counts as Savings?

The final 20% is where real financial progress happens.

Savings can include:

• Emergency fund contributions

• Retirement savings

• Investment accounts

• Paying extra toward debt

According to the Federal Reserve’s Survey of Household Economics, many Americans would struggle to cover an unexpected $400 expense without borrowing. That statistic highlights why consistent saving is critical.

Before investing heavily, most financial planners recommend building an emergency fund first.

You can read more about this in our guide:

How Much Emergency Fund Should You Have

Adjusting the 50/30/20 Budget Rule for Today’s Economy

The traditional 50/30/20 budget rule may feel difficult for people living in expensive cities or dealing with high housing costs.

In those cases, many financial experts recommend modified versions such as:

60/20/20

60% needs

20% wants

20% savings

Or even:

70/20/10 for very tight budgets.

The key principle is not the exact percentages. The real goal is to maintain consistent savings while preventing lifestyle inflation.

Why the 50/30/20 Budget Rule Works

The reason this budgeting method remains popular is its simplicity.

Instead of obsessing over every transaction, the 50/30/20 budget rule focuses on controlling the largest spending categories.

This approach also builds financial habits gradually.

Over time, many people increase their savings rate beyond 20%.

For example:

• 25% savings for aggressive retirement planning

• 30% savings for financial independence goals

But the structure always begins with a simple baseline.

Simple Budget Table

Here is a quick illustration using a $3,500 monthly income.

Income: $3,500

Needs (50%)

$1,750

Wants (30%)

$1,050

Savings (20%)

$700

Even small improvements in spending habits can shift additional money into the savings category.

For example, reducing subscription services or dining out can quickly free up $100–$300 per month.

Tools That Can Help You Follow the 50/30/20 Budget Rule

Many people use budgeting apps to track spending automatically.

Popular tools include:

• YNAB (You Need a Budget)

• Mint alternatives like Monarch Money

• Rocket Money

These tools categorize expenses and make it easier to see whether spending aligns with the 50/30/20 budget rule.

When the 50/30/20 Budget Rule Doesn’t Work

While the 50/30/20 budget rule is a useful guideline, it does not work perfectly for everyone. In particular, people living in high-cost cities may struggle to keep essential expenses under 50% of their income.

For example, housing alone can exceed 50% of take-home pay in cities like San Francisco, New York, or Los Angeles. According to data from the U.S. Bureau of Labor Statistics, housing is the largest expense for most American households and can consume over one-third of total spending.

If your essential expenses exceed 50%, the key is not abandoning the rule entirely but adapting it.

For example:

Modified Budget Example

Needs: 60%

Wants: 20%

Savings: 20%

Or

Needs: 70%

Wants: 20%

Savings: 10%

The principle behind the 50/30/20 budget rule is flexibility. The goal is simply to create structure around spending while maintaining a consistent savings habit.

50/30/20 Budget Rule vs Other Budgeting Methods

The 50/30/20 budget rule is popular because of its simplicity, but it is not the only budgeting method available.

Here are a few other common approaches.

Zero-Based Budgeting

Zero-based budgeting assigns every dollar of income a specific purpose. At the end of the month, income minus expenses equals zero.

This method offers precise control but requires more effort and tracking.

Envelope Budgeting

The envelope system divides spending categories into physical or digital envelopes. When the money in a category runs out, spending stops.

This approach works well for people trying to reduce overspending.

Pay Yourself First

This method prioritizes saving before spending. A fixed percentage of income automatically goes into savings or investments before other expenses occur.

Compared with these methods, the 50/30/20 budget rule strikes a balance between simplicity and structure, making it an ideal starting point for beginners.

One of the biggest advantages of the 50/30/20 budget rule is how easy it is to calculate.

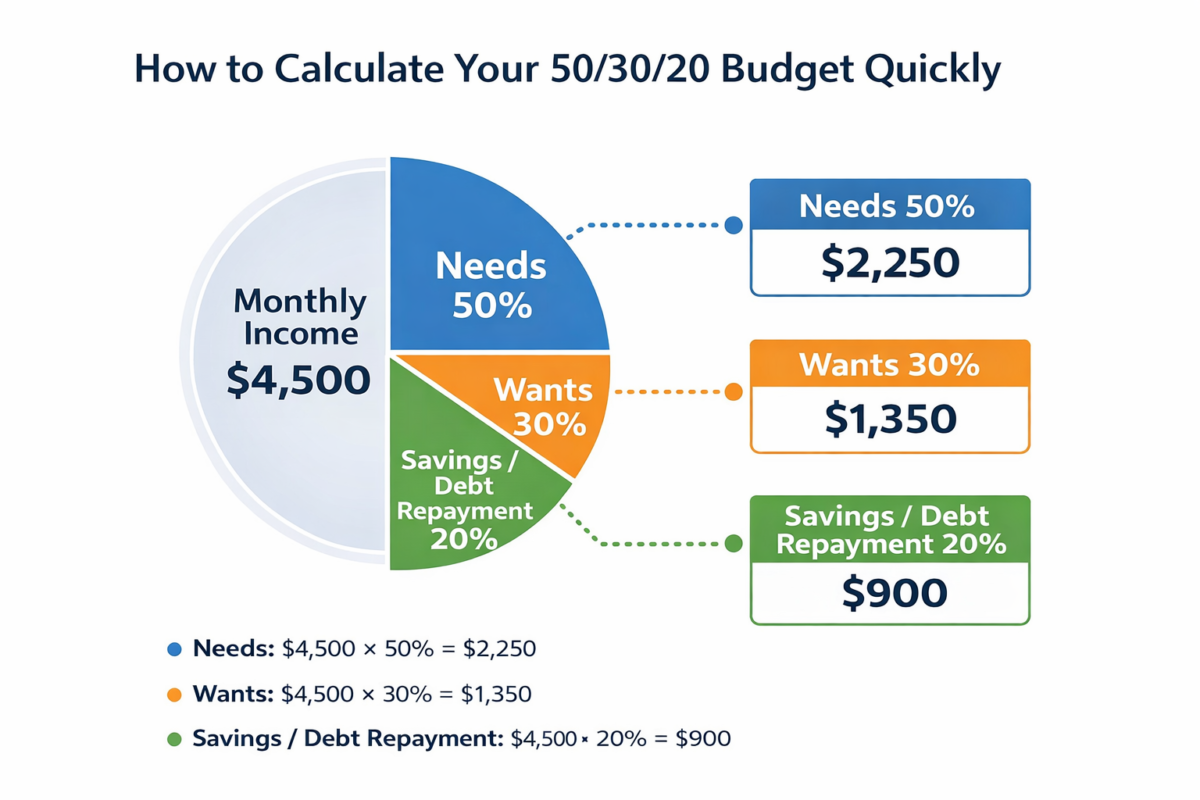

How to Calculate Your 50/30/20 Budget Quickly

Step 1

Determine your monthly take-home income after taxes.

Step 2

Multiply your income by each percentage.

Example of how the 50/30/20 budget rule divides a $4,500 monthly income into needs, wants, and savings categories.

This visual example shows how the 50/30/20 budget rule divides income between needs, wants, and savings.

These numbers give you a clear spending framework that keeps your financial priorities balanced.

If you’re unsure how much you should be saving overall, our guide How Much Money Should You Save Each Month explains common savings benchmarks.

Many financial planners also recommend the 50/30/20 budget rule as a simple starting point for beginners.

Using the 50/30/20 Budget Rule When You Have Debt

Many people wonder whether the 50/30/20 budget rule still works if they have student loans or credit card debt.

The answer is yes, but the savings category may shift slightly.

The 20% portion can include:

• Emergency fund contributions

• Retirement savings

• Extra debt payments

For example:

Savings / Debt Category (20%)

$300 emergency fund

$300 extra loan payments

$200 retirement contributions

Paying down high-interest debt quickly often provides the best financial return.

Once debt is reduced, more of that 20% can shift toward investments and long-term savings.

Why the 50/30/20 Budget Rule Is a Strong Starting Point

The biggest advantage of the 50/30/20 budget rule is that it creates a simple financial structure.

The Consumer Financial Protection Bureau also recommends budgeting as one of the most important tools for improving financial stability.

Many people struggle with money because they lack clear spending boundaries. By dividing income into needs, wants, and savings, this rule prevents lifestyle inflation while encouraging consistent saving.

Even small improvements in savings habits can make a huge difference over time.

For example, saving $500 per month adds up to $6,000 per year and $60,000 over a decade before investment growth.

If you are currently working toward building your first financial safety net, you may also want to read How Much Emergency Fund Should You Have, which explains how large an emergency fund should be based on income stability.

Final Thoughts on 50/30/20 Budget Rule

The 50/30/20 budget rule is not about restricting your lifestyle. Instead, it provides a simple structure for managing money in a way that balances present needs with future financial security.

By dividing income into three clear categories—needs, wants, and savings—you create a system that encourages responsible spending while building long-term stability.

If you are just beginning your financial journey, these guides can help you continue building a strong foundation.

How Much Money Should You Save Each Month

How to Save Money on a Low Income

How Much Emergency Fund Should You Have

Each of these strategies builds on the same core principle: consistent, intentional financial habits lead to long-term stability and freedom.

FAQ

Is the 50/30/20 budget rule realistic?

For many households, it provides a helpful starting structure. However, individuals in high-cost areas may need to adjust the percentages.

Does the 20% include retirement savings?

Yes. Most financial planners include retirement contributions as part of the 20% savings category.

What if my expenses exceed 50% of income?

You may need to temporarily adjust the rule. Focus on reducing discretionary spending while gradually increasing savings.

Further your savings journey here:

How Much Money Should You Save Each Month

How to Save Money on a Low Income

How Much Emergency Fund Should You Have

Together, these strategies form the core of a sustainable financial plan.