")

Learning how to start saving money in your 20s is one of the most important financial skills you can build early in life. Your twenties are when habits form, income begins to grow, and small financial decisions can compound dramatically over time.

Many people assume saving money requires a high salary, but the truth is that learning how to start saving money in your 20s is more about systems than income. With the right approach, even small contributions can build meaningful financial security.

Why Saving in Your 20s Matters

Your 20s are a critical window to start building financial habits. This is when inflation is still cooling (CPI was ~2.4% in early 2026) and your income is likely rising—but you also face big expenses. Over 46 million Americans hold student loans (totaling ~$1.85 trillion). For many young adults, rent consumes 30% or more of income. The earlier you start saving, the more time your money has to grow. In fact, NerdWallet notes that saving just $14 per day from age 23 could accumulate over $1 million by retirement. Those who delay need to save dramatically more later to catch up. The lesson: even small consistent savings now add up with compound interest and time.

Set a Realistic Savings Goal

First, decide a target that’s doable. A common guideline is to save at least 10–15% of your income for both short- and long-term goals. Some experts (like Fidelity Investments) even suggest aiming for 15% each year. On $40,000/year (about $3,000/month take-home), that’s $450/month. If that’s too much at first, start lower and gradually increase. Translate that into a weekly habit: $450/mo ≈ $105/week. Automate transferring that amount each paycheck. Even $25/week adds up: Investopedia estimates that can build a four-digit cushion in one year.

Your goal should include retirement, emergency savings, and debt payoff. For example, apply the 50/30/20 rule: 20% to savings (retirement + emergency fund) and debt. On a $3,000 income, 20% is $600/month. Try reaching that slowly: save 10% now and bump up to 20% over a few years. The important part is forming the habit of “paying yourself first.”

Make Saving Automatic

Leverage technology. Set up automatic transfers so you never see the money. Many banks and payroll systems let you split a direct deposit. Have part go to checking, part to savings. Another option: use an app (like Qapital, Chime, or even traditional bank rules) that automatically moves a percentage of every deposit into savings. This way, saving becomes as routine as paying rent. Investopedia calls this “set-it-and-forget-it” – it removes willpower from the equation.

Also, take advantage of windfalls. For example, allocate a portion of any tax refund, bonus, or gift directly to savings. The IRS lets you split your refund among up to three accounts, so you could send $2,000 of your refund to a high-yield savings account and the rest to checking. Treat a large bonus or gift the same way. Even occasional lumps quickly bolster your balance.

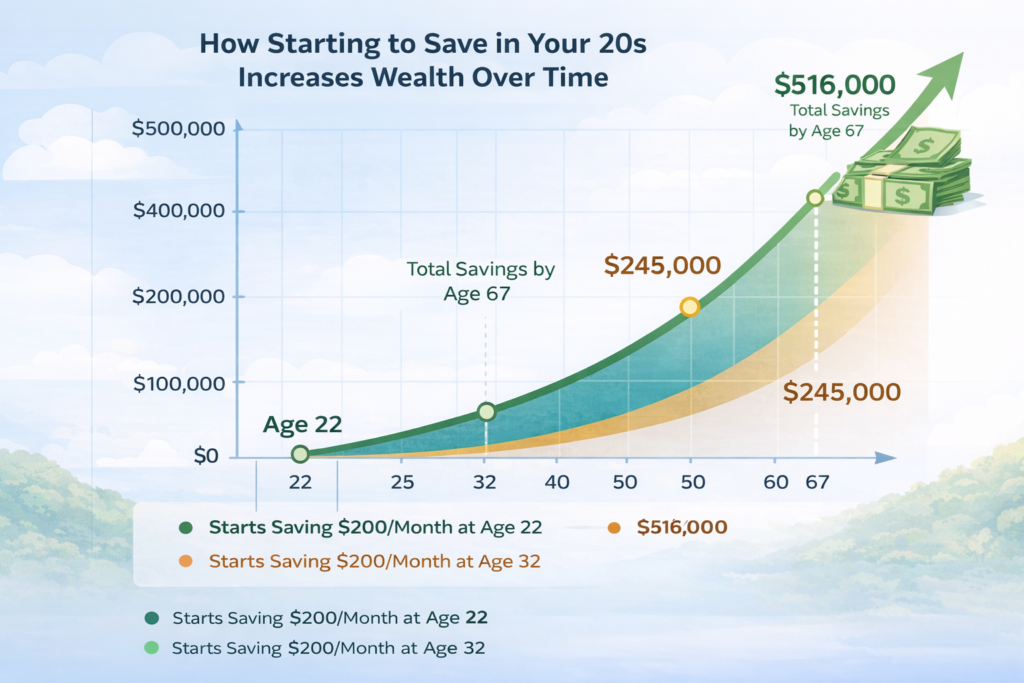

Why Learning How to Start Saving Money in Your 20s Matters

The earlier you begin saving, the more time your money has to compound. For example, someone who saves $200 per month starting at age 22 can end up with significantly more wealth than someone who starts at 35—even if the later saver contributes more money.

According to research from the Federal Reserve, many Americans struggle to cover unexpected expenses, which makes building savings early especially important.

Starting early helps you:

• Build an emergency fund

• Avoid high-interest debt

• Invest earlier for retirement

• Reduce financial stress later in life

If you’re also figuring out monthly savings targets, read our guide on How Much Money Should You Save Each Month.

Practical Steps for How to Start Saving Money in Your 20s

(Each tactic includes a quick example and how long to reach a savings milestone.)

- Automate $25/week → $1,200/year: Set $25 automatic weekly transfer. In one year that’s $1,200 (enough for a starter emergency cushion). After 10 years, that’s $12,000 plus interest. (Time to $5K: ~4 years.)

- Use employer match: Contribute to your 401(k) up to the employer match. E.g., 6% of a $40K salary is $2,400+ match. (Instant return: 100%. Time to $5K: ~2 years counting only your contributions.)

- Side gig boost ($150/week): Work a few evening hours for an extra $150/week (~$600/month). Save this entire side income. (Adds $7,200/year. Time to $10K: ~1.5 years on side income alone.)

- No-spend challenges: One day a week, no extra spending (coffee, lunch out, etc.). If you normally spend $10/day on lunch, a no-spend day saves $50/month. (Time to $5K: ~8 years with just $50/mo, but combine with others.)

- Round-up savings apps: Use apps like Acorns that round purchases to the next dollar and save the change. If you spend $30/day, that’s ~$0.70 each day to savings = $21/month. (Time to $1K: ~4 years, but builds a habit.)

- Student perks: If in school, use student discounts, scholarships, and on-campus jobs. Put all scholarship money directly into savings. Even $100/month in grants + $100 in part-time pay = $2,400/year. (Time to $5K: ~2 years at $200/mo.)

- High-yield savings account: Keep your fund in an account earning ~4–5% APY. On $3,000, 5% yields $150/year vs $3 at 0%. Over several years, those extra dollars add up. (Not a huge one-year impact, but builds over time.)

- Budgeting frameworks: Follow the 50/30/20 or a zero-based budget. If you usually spend everything, the act of categorizing helps find cuts. For example, limiting eating-out to $100/mo could instantly free $200. (Time to $5K: ~2 years at $200/mo.)

Mix and match these tactics based on your situation. A student might prioritize no-spend days and small part-time jobs. An early-career professional might focus on employer retirement match and automated transfers. The key is consistency: small habits compound.

Tools to Supercharge Your Savings

Use technology to track and grow your savings:

| Name | Cost | Key Feature | Affiliate Tip |

|---|---|---|---|

| High-Yield Savings Account (e.g. Ally Bank) | Free/open | Earns ~4–5% APY; FDIC-insured | Unspecified (look for bank partners) |

| Budgeting App (e.g. Mint, YNAB) | Free / premium | Tracks spending and savings goals automatically | Unspecified (some apps have referral) |

| Round-Up App (Acorns, Qapital) | $1–$5/month | Rounds purchases to invest or save spare change | Unspecified (common affiliate) |

Choose tools that automate saving and fit a tight student/young adult budget (no monthly fees is key).

FAQ

- How to Start Saving Money in Your 20s?

Aim for 10–20% of your income as a starting range. For example, saving 10% of a $3,000 monthly net income is $300. If possible, work up to higher levels (e.g. Fidelity’s 15% guideline) as your income grows. Even a small percentage is beneficial; consistency matters more than hitting a perfect number. - Can a college student really save money?

Yes. Students can start with tiny amounts. Use automatic transfers when you get paid (stipends, part-time wages). Take advantage of student discounts on essentials to reduce spending. Every few dollars saved adds up: Investopedia notes “Even $25 a week can build a four-figure cushion in a year.” - Should I pay down debt or save first?

Balance both. Keep a small “starter” emergency fund ($500–$1,000) while making minimum payments on debt. After that, split extra funds: put half toward loans and half into savings or retirement. At minimum, capture any employer 401(k) match – it’s like a guaranteed 100% return – even while paying down loans. - What if I have unpredictable income (gig work)?

If your income varies, use percentage-based rules. Save, say, 10% of every payment, or use an app that auto-saves a percentage. Also, maintain a larger buffer in savings to handle lean months. Treat savings as a “zero-based” budget item so it’s prioritized whenever money comes in. - Where is the best place to keep my savings?

Put short-term savings (emergency fund, near-goals) in a safe, liquid place: a high-yield savings account or money market. For long-term goals, use tax-advantaged accounts (401(k), IRA) or brokerage accounts. The important part is separation: keep savings in an account you won’t touch on a whim. - Is saving in small amounts worthwhile?

Yes! Starting early, even small amounts, benefits from compound interest over decades. NerdWallet’s example shows saving $14/day from 23 leads to a $1M retirement fund. If you wait, you must save much more later to reach the same goal.

Financial Research on Saving Early

Financial experts consistently emphasize the importance of saving early in adulthood. Research from institutions such as:

• Federal Reserve – https://www.federalreserve.gov

• Harvard Business School – https://www.hbs.edu

• Wharton School of Finance – https://www.wharton.upenn.edu

These institutions highlight three core principles:

• Start saving early to utilize compound interest

• Automate contributions

• Increase savings as income grows

Final Thoughts

Related posts: How Much Money Should You Save Each Month; How Much Emergency Fund You Need. Feel free to explore these for more budgeting strategies and emergency savings guidance.

In How to Start Saving Money in Your 20s — Saving money in your 20s is as much about forming habits as it is about the dollar amount. Start with realistic steps: set aside even a small fixed percent or weekly sum, automate it, and build from there. Use tools and incentives (like 401(k) matches and apps) to make saving automatic. Over time, those habits grow into real wealth. The discipline you build now – living on a little less than you earn – will pay off far more than any single balance today.