For many households, tax season brings the biggest lump sum of money they will see all year. That is exactly why knowing how to use your tax refund matters so much.

A tax refund can feel like free money, but it is usually better viewed as an opportunity. Used strategically, it can help you stabilize your finances, reduce stress, build savings, and make faster progress toward long-term goals. Used impulsively, it can disappear in a week and leave you in the exact same position you were in before.

If you are wondering how to use your tax refund in today’s economy, this guide will walk you through a practical order of operations that makes sense for real life. The goal is not to shame you out of enjoying any of it. The goal is to help you use your refund in a way that actually improves your financial position.

That matters even more right now. Even though inflation has cooled from its highs, many households still feel squeezed by groceries, rent, insurance, utilities, and debt payments. In that kind of environment, a tax refund should not just be spent. It should be assigned a purpose.

Why Your Tax Refund Deserves a Plan

The reason so many people search for how to use your tax refund is simple: a lump sum creates choices.

You can spend it.

You can save it.

You can pay off debt.

You can split it across multiple priorities.

The problem is that without a plan, most refunds get absorbed by random spending, delayed bills, subscriptions, eating out, online shopping, and small purchases that feel harmless in the moment. A month later, the money is gone and the deeper issues are still there.

The smarter move is to decide in advance what job your refund needs to do. That starts with one question:

What would improve my financial life the most over the next 6 to 12 months?

For one person, that might be starting an emergency fund. For another, it might be wiping out high-interest credit card debt. For someone else, it might be catching up on bills, fixing a cash flow problem, or investing for retirement.

The right answer depends on your current financial reality, not social media advice.

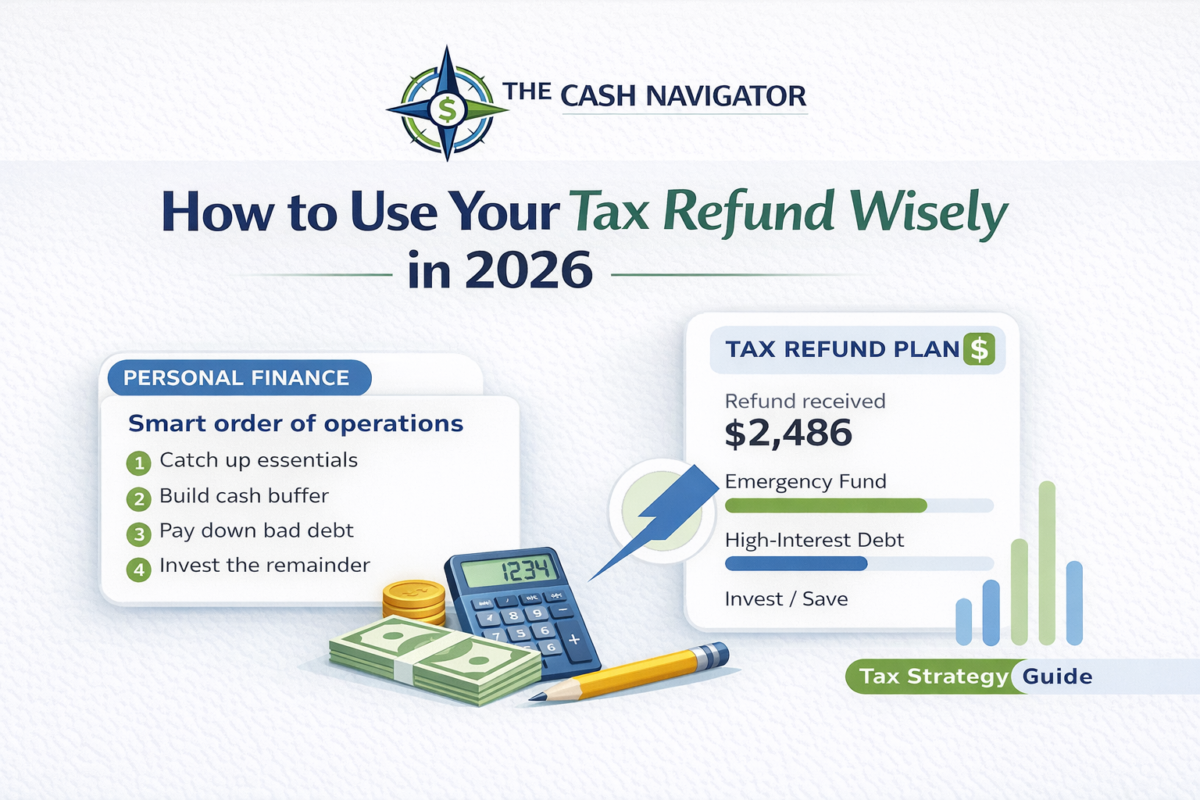

The Best Order of Operations for Your Tax Refund

If you want the simplest answer to how to use your tax refund, use this order of operations:

- Cover urgent essentials

- Build or strengthen your emergency fund

- Pay down high-interest debt

- Catch up on critical obligations

- Invest for long-term goals

- Use a small portion for enjoyment if your core priorities are handled

This framework works because it balances stability, flexibility, and progress. It is not all-or-nothing, and it helps you make decisions that will still feel smart three months from now.

Step 1: Cover Urgent Essentials First

The first rule of how to use your tax refund is this: if your finances are under pressure, stabilize the basics first.

That can include:

- Overdue rent or mortgage payments

- Utilities that are behind

- Groceries and household necessities

- Critical car repairs needed for work

- Insurance premiums that protect you from bigger risk

- Minimum payments that keep accounts current

This may not feel exciting, but it is often the highest-return move. Financial stability starts with keeping the lights on, protecting housing, and preventing a temporary problem from turning into a crisis.

If this is where your refund needs to go, that does not mean you wasted it. It means you used it to protect your foundation.

Step 2: Build a Starter Emergency Fund

If your basic needs are covered, the next best answer to how to use your tax refund is often emergency savings.

Why? Because a tax refund can help break the cycle of using credit cards for every surprise expense. One car repair, one vet bill, one medical visit, or one appliance breakdown can throw off an entire month if you do not have cash reserves.

If you do not have an emergency fund yet, your refund is one of the best ways to start one fast.

A practical sequence looks like this:

- First goal: $500

- Second goal: $1,000

- Third goal: one month of essential expenses

- Longer-term goal: three to six months of core expenses

You do not need to hit the final number immediately. The point is to create a cash buffer that makes your life less fragile.

Helpful internal resources:

- How Much Emergency Fund Should You Have?

- How to Save Your First $1,000

- Live Happy Using the 50/30/20 Budget Rule

If you already have some emergency savings, your refund can help strengthen it. In an economy where people still feel the pressure of higher everyday costs, cash on hand buys breathing room.

Step 3: Pay Down High-Interest Debt

Another strong answer to how to use your tax refund is to reduce high-interest debt, especially credit cards.

High-interest debt quietly drains your income every month. Even if you are making minimum payments, the interest can keep balances hanging around much longer than people expect. Using a tax refund to knock down those balances can improve your monthly cash flow and reduce total interest paid.

This is especially useful if your refund can:

- Pay off a smaller balance completely

- Cut a large balance enough to reduce utilization

- Eliminate a card with a high minimum payment

- Stop the need to revolve debt month after month

If you are debating whether savings or debt should come first, the answer depends on your situation. In many cases, the smartest approach is a split: keep a small emergency cushion, then put the rest toward high-interest debt.

Helpful internal links:

- How to Get Out of Debt Fast

- What Is a Good DTI? (And How to Lower Yours Fast)

- Debt-to-Income Ratio Calculator

If your balances are heavy and your savings are low, a refund can be the reset button that helps you move from reactive to intentional.

Step 4: Catch Up on Important Financial Maintenance

Sometimes the best use of a refund is not traditional saving or investing. Sometimes it is financial maintenance.

This can include:

- Replacing worn tires before they become unsafe

- Handling preventive dental or medical costs

- Catching up on essential home maintenance

- Paying annual insurance costs

- Fixing something that has been causing recurring expenses

This still counts as using your refund wisely.

A lot of personal finance advice is too rigid. Real life is not always save everything or invest everything. Sometimes the best answer to how to use your tax refund is spending it on something that prevents a much bigger problem later.

Step 5: Invest If Your Foundation Is Already Solid

If your emergency savings are in decent shape and high-interest debt is under control, then how to use your tax refund becomes a wealth-building question.

At that point, your refund can be used to:

- Contribute to a Roth IRA or traditional IRA

- Add to a brokerage account

- Increase 401(k) contributions and use the refund to support cash flow

- Invest in a long-term diversified portfolio

This is where a refund stops being just extra money and starts becoming capital.

Even a modest one-time investment can matter when it is added to a broader system of consistent saving. The key is making sure the basics are handled first. Investing while you are one emergency away from new credit card debt is usually not the strongest move.

Helpful internal resources:

Step 6: Split the Refund on Purpose

One of the best answers to how to use your tax refund is not choosing just one category. It is splitting the money deliberately.

For example, a refund could be divided like this:

- 50% to emergency savings

- 30% to high-interest debt

- 20% to a personal or family goal

Or like this:

- 40% to catching up on bills

- 40% to a credit card payoff

- 20% to enjoyment or discretionary spending

Or like this:

- 60% to an IRA

- 20% to short-term savings

- 20% to a home or car maintenance fund

This approach works well because it gives your refund multiple jobs without blowing the whole thing on one impulse decision.

It also reflects reality: many people need both relief and progress. A split-refund mindset can be much more sustainable than forcing yourself into an extreme choice you will resent.

Do Not Treat Your Refund Like Free Money

A major mistake people make when deciding how to use your tax refund is mentally treating it like a bonus that appeared out of nowhere.

In most cases, your refund is money that came back to you after withholding and credits were calculated. That is why it deserves the same level of intentionality as a paycheck.

If you are receiving a larger refund than usual, use that as a chance to improve your system, not just your shopping list.

That can mean:

- Reducing one of your biggest financial pain points

- Creating a buffer that lowers anxiety

- Improving monthly cash flow

- Building net worth more efficiently

What About Spending Some of It for Fun?

Yes, that can be reasonable.

If you are asking how to use your tax refund, the smartest answer does not have to be joyless. If your essentials are covered and you have assigned most of the refund to meaningful goals, using a small percentage for enjoyment is fine.

That might mean:

- A modest weekend trip

- A family experience

- Upgrading something you use every day

- Buying something intentional rather than random

The key is setting the amount in advance. Enjoying 10% to 20% of your refund is very different from watching 100% disappear without improving your financial life at all.

How to Decide What Your Refund Should Do

If you still are not sure how to use your tax refund, run through this checklist:

- Am I behind on any essential bills?

- Do I have at least a starter emergency fund?

- Do I have high-interest debt costing me every month?

- Is there a critical repair or obligation I have been delaying?

- Am I ready to invest because my basics are already strong?

- Do I want to split the refund across multiple priorities?

The first yes often tells you where the money should go.

A Smart Tax Refund Example

Here is a practical example of how to use your tax refund if you receive $2,400:

- $1,000 to emergency savings

- $900 toward a high-interest credit card

- $300 for a car maintenance fund

- $200 for something enjoyable

That one refund improves stability, reduces interest costs, prepares for future expenses, and still leaves room for enjoyment.

That is the kind of structure that changes your trajectory instead of just your mood for a weekend.

Make Next Year Easier Too

There is one more useful angle to how to use your tax refund: use this year’s refund to make next year less stressful.

You can do that by using part of it to:

- Create a sinking fund for irregular bills

- Build a true emergency fund

- Lower debt payments

- Automate savings after each paycheck

- Strengthen your overall personal finance system

That way, your refund is not just solving today’s problem. It is helping future you operate with more control.

Helpful related reading:

- The 50/30/20 Budget Rule Explained

- Live Happy Using the 50/30/20 Budget Rule

- Best Budgeting Apps in 2026

Final Thoughts: The Best Tax Refund Plan Is the One That Improves Your Life

The best answer to how to use your tax refund is not always flashy. Usually, it is practical.

Use your refund to strengthen your finances where they are weakest. That might mean stabilizing bills, building savings, attacking debt, handling neglected maintenance, or investing for the future.

The point is not to be perfect. The point is to be intentional.

A tax refund is one of the few moments in the year when you can make a meaningful move all at once. Treat it like an opportunity to reduce stress, increase flexibility, and build momentum.

If you do that, your refund can become more than a temporary boost. It can become a turning point.

Leave a Reply